Modern buyers have turned real estate into a performance sport, and the scoreboard is making them miserable. There is a specific kind of buyer I encounter constantly now. Usually intelligent. Usually financially literate. They read market reports recreationally. They know where mortgage rates were three Thursdays ago. They have spreadsheets, alerts, opinions about inventory trends, and a running internal monologue about whether they should have bought six months earlier.

And despite all of this information — or more accurately, because of it — they are unable to move.

What’s striking is that the paralysis rarely comes from a lack of affordability or preparation. Most of the time, it comes from something far more difficult to admit. Beneath the spreadsheets and the market analysis sits a quieter question, one that almost nobody says out loud because it sounds irrational once spoken plainly:

"What if I make the wrong move and everyone can see it afterward?"

This is the psychological shift that has transformed modern home buying. People no longer experience real estate simply as shelter, stability, or even investment. Increasingly, they experience it as public evidence of their judgment. The purchase is no longer just a purchase. It becomes a referendum on intelligence, timing, discipline, status, and financial sophistication.

And once a home becomes a scorecard, peace becomes almost impossible.

THE SCOREBOARD NEVER STOPS UPDATING

Twenty years ago, most people bought homes with incomplete information and a fairly simple framework. You bought because your life required it or because your finances allowed it. The exact timing mattered, of course, but mostly as a practical consideration. The price was a constraint, not a moral verdict.

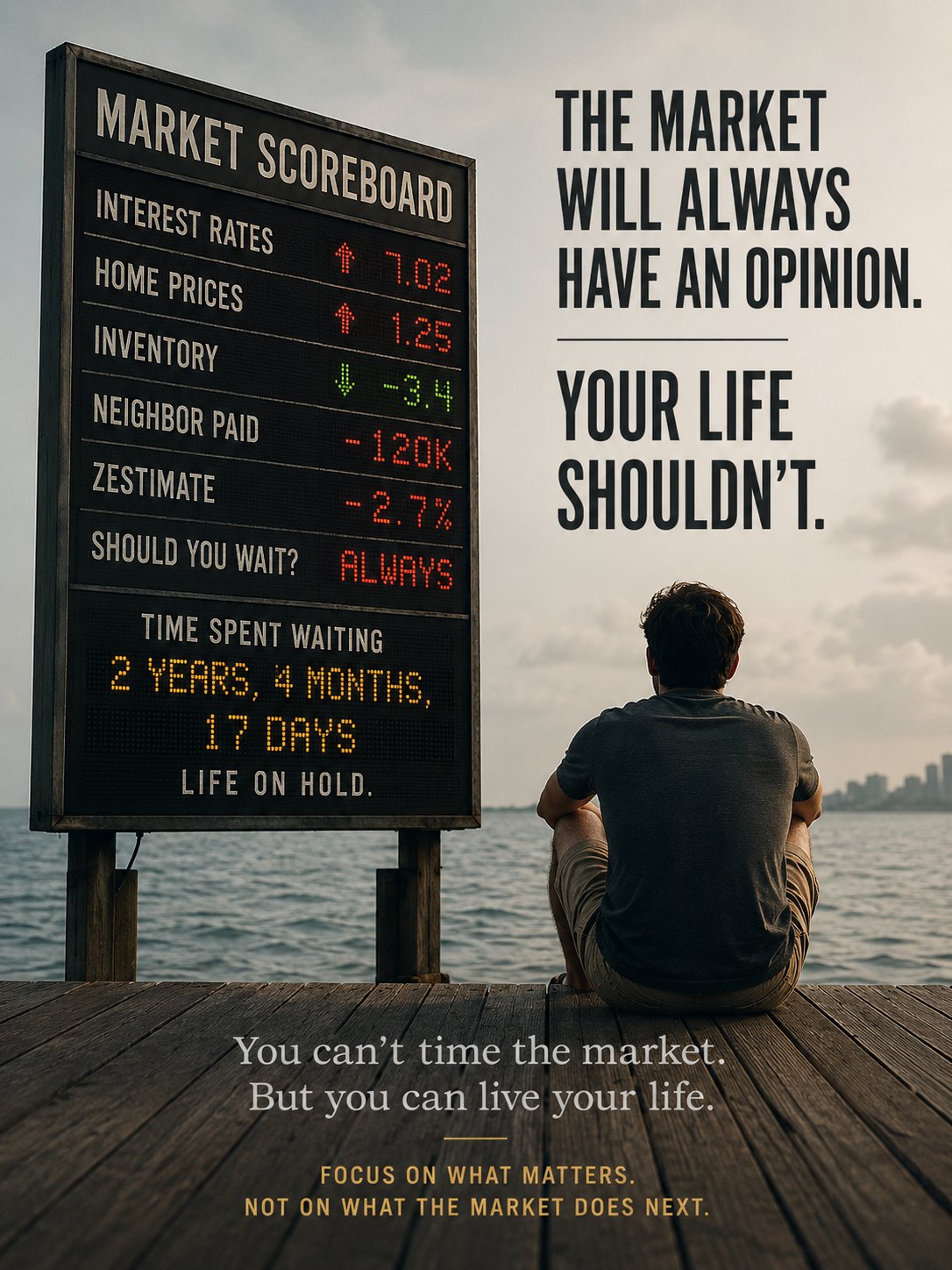

Now, the entire experience has been 'financialized', quantified, and made relentlessly public. Buyers track 'Zestimates' the way investors track earnings reports. They monitor interest rates like traders watching futures markets. They scroll through listing histories searching for evidence that someone else negotiated better than they did. They know what their neighbors paid in 2021 and what their coworker refinanced into in 2020. They compare purchases across timelines that never actually coexisted and then emotionally react as though they somehow failed an exam. The problem is not simply access to information. The problem is the emotional meaning people attach to it.

A buyer closes on a home they genuinely love, one they can comfortably afford, in a neighborhood that improves their daily life. Six months later, rates move or prices soften slightly, and suddenly the entire experience feels contaminated. They begin rerunning imaginary scenarios in their heads. If they had waited another quarter. If they had bought two years earlier. If they had negotiated harder. If they had been “smarter.” What they are really doing is converting hindsight into self-judgment. This is why the modern obsession with “overpaying” often has very little to do with the actual house.

WHAT PEOPLE MEAN WHEN THEY SAY THEY “OVERPAID”

Ask buyers whether they are afraid of overpaying and they will usually answer with economic language. They will talk about rates, inventory, price trajectories, and macro conditions; but, listen carefully and most of the fear is social and psychological long before it is mathematical. In practice, many people now define “overpaying” as any situation in which the market moves against them after closing, even temporarily. A comparable property sells for less a year later? They overpaid. Mortgage rates improve after they lock? They overpaid. Someone in their social circle bought a similar house at a lower price years earlier? They definitely overpaid.

None of those things necessarily indicate a bad purchase. They indicate that markets move and timing is imperfect.

Timing has become emotionally loaded because buyers increasingly interpret market fluctuations as reflections of personal intelligence. People do not just want their purchase to work financially. They want it to look smart historically. That is a very different psychological burden. The word “overpaying” often functions as socially acceptable language for something much more uncomfortable: the fear of looking foolish in hindsight. And hindsight, unfortunately, is undefeated.

WHAT REAL OVERPAYING ACTUALLY LOOKS LIKE

Real overpaying has much less to do with temporary market movement than people imagine: it happens when the purchase fundamentally destabilizes your life rather than supporting it. It happens when the monthly payment creates chronic stress instead of predictable structure. When someone buys a long-term asset with a short-term horizon and then acts surprised when the math becomes painful. When the property fits an aspirational identity better than it fits actual daily life. When major structural problems are ignored because emotion overwhelmed judgment. When a buyer stretches so aggressively to acquire the house that the house quietly takes ownership of them instead.

That is real overpaying.

A 'Zestimate' decline is not necessarily overpaying. A temporary market correction is not necessarily overpaying. A different interest rate environment six months later is not necessarily overpaying. Those are market conditions. They are not moral verdicts. The more useful question is far simpler: did the purchase create stability, or did it create strain? And. Most people already know the answer to that question long before the market tells them anything.

THE FANTASY OF THE PERFECT ENTRY POINT

There is another layer to this psychology that has become especially powerful over the last few years: the widespread belief that a major correction is always just around the corner. You hear versions of it constantly now. Buyers talk about “waiting for the crash” as though the market is standing backstage preparing for its cue. The assumption is that patience will eventually be rewarded with a clean, obvious moment to enter — a moment when prices are lower, risk feels minimal, and everyone collectively agrees that now is finally safe. Maybe prices will soften further in some markets. Some already have. Real estate is not immune to cycles, and pretending otherwise is intellectually unserious.

What many buyers misunderstand is that falling prices do not usually create emotional confidence. More often, they create emotional fear. When markets are rising, people fear being priced out. When markets are falling, they fear catching a falling knife. The emotional discomfort simply changes costumes. The same buyer confidently claiming they will purchase after a correction often becomes dramatically more hesitant once negative headlines appear, layoffs increase, financing tightens, or uncertainty becomes tangible instead of theoretical. The imagined correction feels empowering from a distance. Living inside one feels very different.

And even when prices do decline, the financial reality is frequently less transformative than people expect. A modest drop in price does not necessarily offset higher borrowing costs, years spent delaying life plans, rising rents, lost time, or the psychological fatigue of remaining in a constant state of “almost ready.” This is the part buyers rarely account for: many people are not actually waiting for better numbers. They are waiting for the emotional experience of certainty--the market almost never provides it. There is no universally approved entry point. No moment where risk disappears and everyone agrees the decision was brilliant. No headline announcing that buyers may now proceed without the possibility of regret.

That moment does not exist.

THE MARKET IS NOT EVALUATING YOUR CHARACTER

Somewhere along the way, people began treating market performance as evidence of personal worth. A temporary decline in value became proof of bad judgment. A missed low-rate window became evidence of failure. A purchase near the peak of a cycle became something to confess apologetically, as though the buyer had violated some objective law of intelligence. Markets are not designed to validate your identity. They are simply systems that move.

Every asset class behaves this way. Investors understand this perfectly well when discussing someone else’s portfolio. They understand volatility intellectually. They understand cycles conceptually. Yet many people lose that perspective entirely once the asset becomes their own home and, by extension, part of their self-image. A home purchased at the 'wrong' point in a cycle is not automatically a bad decision. Sometimes it is simply a life decision made during imperfect market conditions, which is how most real estate decisions throughout history have actually occurred.

In my experience, the buyer terrified of “overpaying” today often becomes the seller insisting their own home is worth more than the market says tomorrow. Which tells you something important:

-The issue was never purely mathematical.

-The market number stopped feeling informational and started feeling personal.

-There is no such thing as perfectly timed participation in a market that is constantly moving. There are only decisions made with incomplete information under changing conditions.

-The people waiting for absolute certainty are not escaping this reality. They are simply postponing their participation in it.

THE COST OF WAITING IS STILL A COST

This is the genuinely uncomfortable part: the buyers most obsessed with avoiding regret often end up organizing entire years of their lives around the avoidance of emotional discomfort. They postpone neighborhoods they wanted to live in, schools they wanted their children to attend, space they needed for relationships and family, routines they were ready to build. Life enters a holding pattern while they continue searching for a version of the market that feels psychologically risk-free. Eventually, many of them buy anyway, often under different conditions than the ones they originally waited for. Sometimes at higher prices. Sometimes with higher rates. Almost always carrying the exhaustion that comes from spending years mentally rehearsing a decision instead of making one.

And the irony is difficult to miss: the regret they spent years trying to avoid — the fear that they should have acted sooner — frequently arrives anyway. Only now it arrives with additional lost time attached to it.

THE REAL QUESTION

Most buyers think their hesitation is analytical. Usually it is emotional analysis disguised as financial discipline. The real question is not whether you purchased at the exact bottom of the market. Almost nobody does. The real question is whether you bought the right thing, for the right reasons, at a payment you could realistically carry while building the life you actually wanted. If the answer to that question is yes, then temporary fluctuations in the market are just fluctuations. They are not evidence that you failed some invisible intelligence test. The scoreboard will continue updating regardless. Prices will move. Rates will change. Someone somewhere will always appear to have timed things better.

But the market is not living inside the house.

You are.