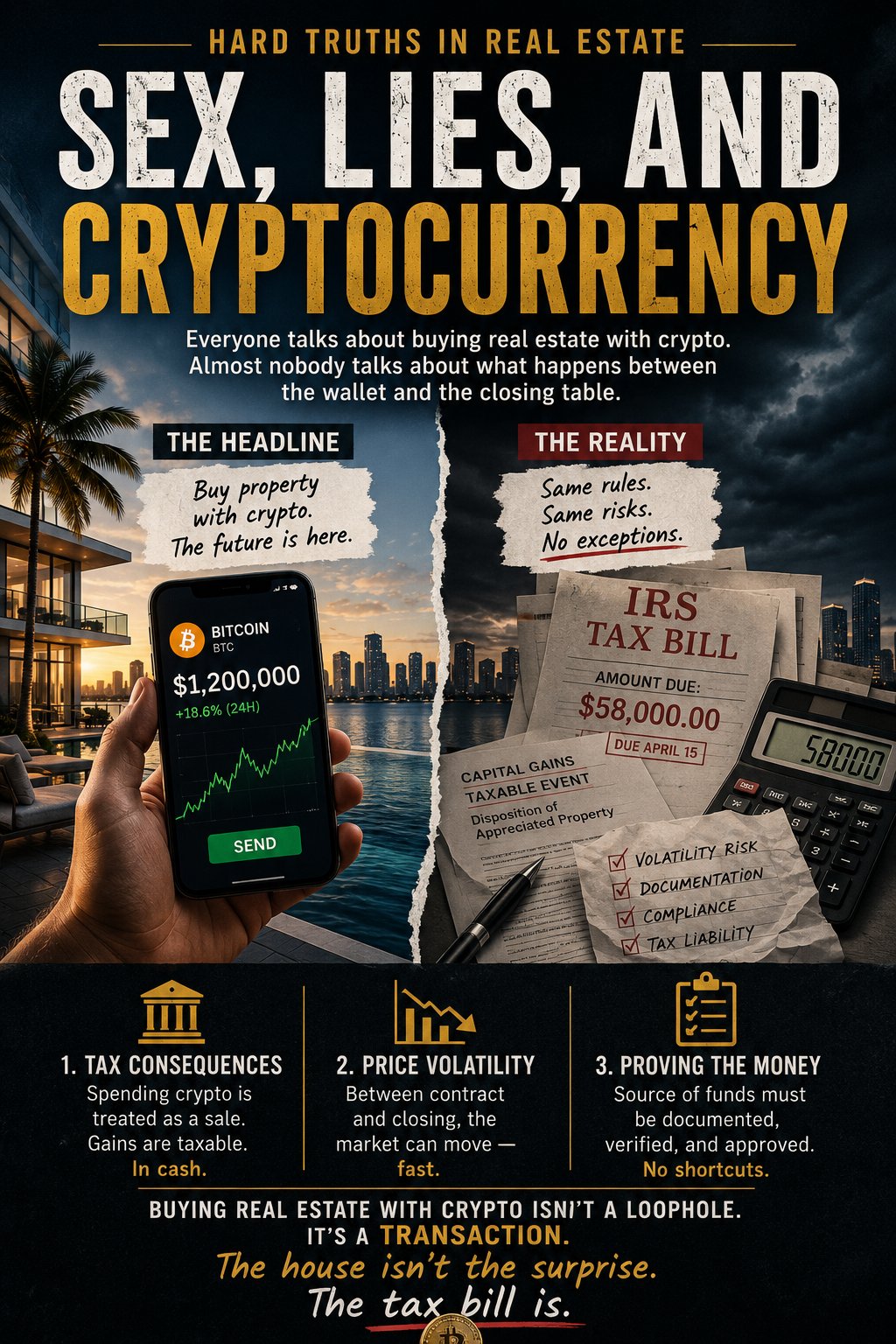

The lie is not that you can buy real estate with crypto. You can. The lie is that crypto somehow exempts you from the rules everyone else follows. That a blockchain transaction is different in kind from a cash transaction. That the IRS sees a wallet address and looks the other way. That the closing table cares what your assets are made of.

It doesn't. They don't. And the people who find this out after closing find it out the hard way.

THE TAX BILL NOBODY SAW COMING

The IRS treats cryptocurrency as property. It means that when you spend Bitcoin to buy a house, the government treats the transaction as if you sold the Bitcoin first — and then used the proceeds to buy the property. The house is the purchase. The crypto is the taxable event.

You never touched cash. You still triggered a gain. And that gain is due — in cash, not crypto — the following April.

CONSIDER SOMEONE WHO

Consider someone who bought $40,000 worth of Bitcoin in 2019. By early 2024, that position had grown to $280,000. They find a Brickell condo listed at $550,000. The seller accepts crypto. They wire the equivalent in Bitcoin and get their keys.

Six months later, their CPA calls.

The IRS treats the transaction as a disposition of appreciated property. The $240,000 gain — the difference between what they paid for the Bitcoin and what it was worth when they spent it — is fully taxable. At long-term capital gains rates plus the 3.8% net investment income tax, the bill lands somewhere in the range of $55,000 to $60,000.

Due in cash. Not crypto. The following April.

They thought the transaction was finished the day they got the keys. It wasn't. It was just beginning.

The house wasn't the surprise. The tax bill was.

And unlike the condo, nobody showed them photos of it beforehand.

This is not a technicality. It is not an edge case. It is the rule, and it applies to every crypto asset used in every real estate transaction. The IRS does not need to see your wallet. It only needs to see the gain.

THE BILL THAT ARRIVES BEFORE CLOSING

The tax liability is the consequence that arrives after. But there is a risk that arrives before — during the thirty to sixty days between contract and closing, while the clock is running and the currency is moving.

RUN THE NUMBERS

You agree to purchase a Coconut Grove home for the equivalent of $1,200,000 in Bitcoin. At contract, Bitcoin is trading at $60,000. You owe 20 Bitcoin.

Thirty days later — a routine closing timeline — Bitcoin drops to $48,000. Your 20 Bitcoin is now worth $960,000.

You are $240,000 short. The seller still wants $1,200,000. The contract still says closing is Friday.

You either come up with the difference in cash, renegotiate under pressure with a seller who has no obligation to cooperate, or you lose the deposit and walk away.

A 20% swing in Bitcoin is not a worst-case scenario. It is a Tuesday.

You are not just buying a property. You are simultaneously holding a position in a volatile asset and racing the clock to close before the math changes — while a tax liability accumulates quietly in the background on whatever gain you are sitting on.

THE THIRD PROBLEM — PROVING THE MONEY IS YOURS

Even before the tax event and the volatility, there is a more immediate obstacle: documentation. Title companies, lenders, attorneys, and compliance departments all ask the same question — where did this money come from? — and they require an answer that can be traced, verified, and signed off on by professionals whose licenses depend on getting it right.

If your assets moved through multiple wallets, decentralized exchanges, or years of layered transactions, that paper trail can become genuinely complicated. You may have earned every dollar legitimately. That does not mean everyone in the transaction can confirm it quickly enough to close on schedule.

WHO THIS ACTUALLY WORKS FOR

The buyers who successfully purchase real estate with cryptocurrency rarely look like the headlines. They are usually already wealthy, already advised, already documented, and already prepared for the tax consequences. They are not using crypto to avoid the system. They are using crypto inside the system.

The people who succeed with crypto real estate are usually the people who needed crypto the least.

Most people score lower than they think.

WHEN IT WORKS

Consider someone else. A software engineer who relocated from San Francisco to Miami in 2022 with an Ethereum portfolio she had been building since 2017. By the time she was ready to buy, her holdings had grown well past what she needed — but liquidating everything meant a tax event she wasn't prepared to absorb in a single year.

Instead, she worked with a CPA to calculate the optimal amount to convert: enough to cover a cash purchase, structured to spread the tax exposure across two fiscal years. She bought a townhouse in Wynwood. She kept the rest of her portfolio intact. She paid what she owed and had planned for it in advance.

The transaction took longer. It required more professionals. It required more paperwork.

But it worked.

The difference between her outcome and the cautionary tales above wasn't cryptocurrency. It was preparation.

Buying real estate with cryptocurrency is not revolutionary. It is not a loophole. It is not a way around the system. It is a transaction — one that happens to involve a volatile, appreciating asset with significant tax consequences that most buyers discover too late.

For a surprising number of them, the house isn't the surprise.

The tax bill is.

If you're sitting on appreciated crypto and thinking about real estate, the most expensive conversation is usually the one you don't have before signing the contract. Let's talk.