Many investors — new and experienced — eventually face the same obstacle:

Their personal income does not align with the traditional underwriting model of banks.

Not because the deal isn’t solid.

Not because they lack experience.

But because conventional financing is structured primarily around personal income.

In a market like Miami — where many investors are business owners, self-employed, commission-based, or strategically structured for tax purposes — that distinction matters.

There are several financing structures that approach underwriting differently.

One of them is the DSCR loan.

This is not a recommendation.

It is a framework — so you can evaluate whether this structure aligns with your strategy.

What Is a DSCR Loan?

DSCR stands for Debt Service Coverage Ratio.

It is an investment property loan where approval is based primarily on the income generated by the property, rather than the borrower’s personal income.

The core question becomes:

Can the property support its own debt?

The formula:

DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment (PITI)

(Principal, Interest, Taxes, Insurance)

A DSCR of 1.00 means the property covers its debt.

Most lenders require somewhere between 1.0 and 1.25.

Instead of evaluating how much you earn today,

the lender evaluates how much the property is expected to generate in the future.

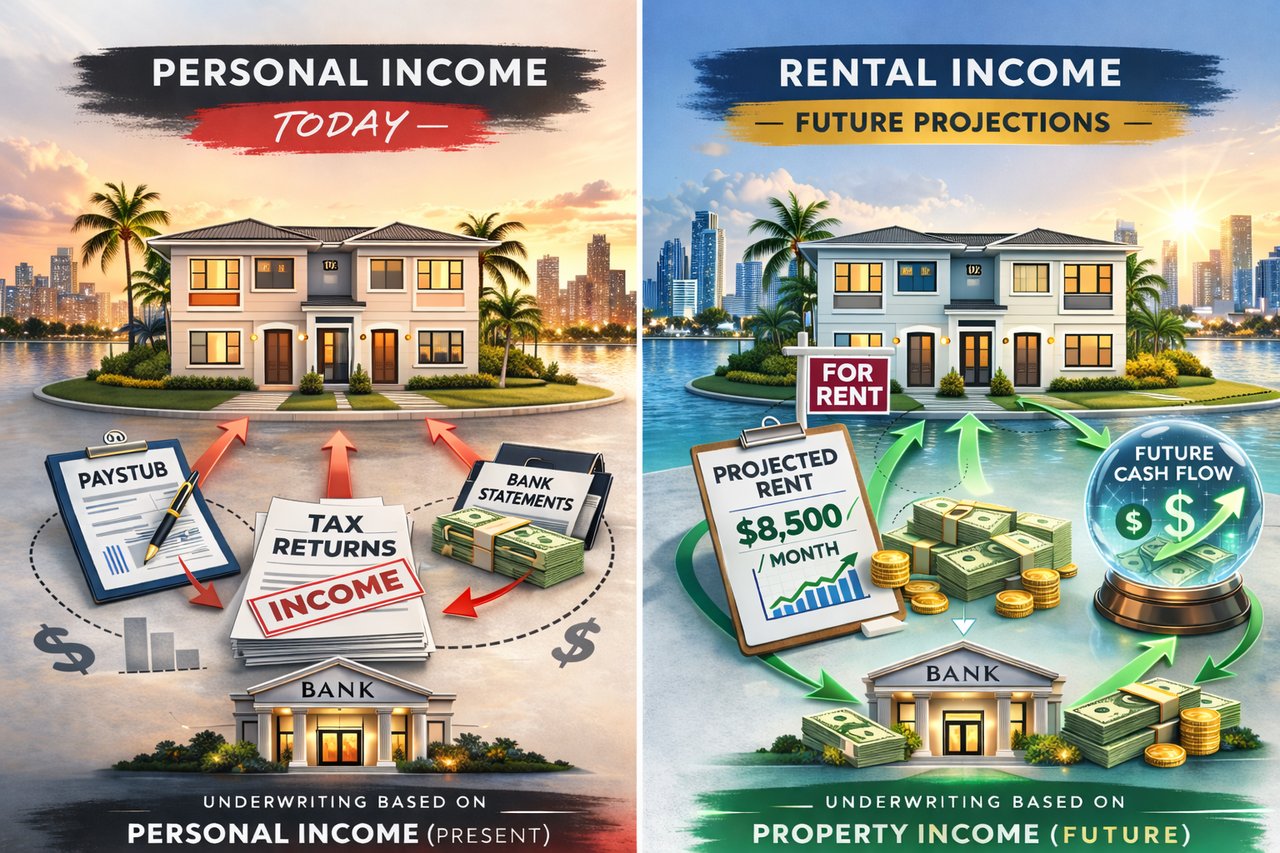

How This Differs from Conventional Investment Loans

A conventional investment loan typically evaluates:

-

Personal income

-

Tax returns

-

Debt-to-income ratio (DTI)

-

Employment history

-

Credit profile

In that model, the bank assesses your personal ability to repay the loan.

With a DSCR structure, the focus shifts to the performance of the asset itself.

Neither approach is inherently superior.

They simply measure risk differently.

A $1,000,000 Miami Example

Consider a realistic scenario:

Purchase price: $1,000,000

Down payment (25%): $250,000

Loan amount: $750,000

Assume an interest rate near 7.5%.

Estimated monthly payment (PITI): approximately $6,800

(Exact figures vary based on taxes and insurance.)

Projected monthly rent: $8,500

Now calculate:

$8,500 ÷ $6,800 = 1.25 DSCR

From a DSCR perspective, the property qualifies.

The projected rental income exceeds the monthly debt obligation.

Under conventional underwriting, however, the lender would also evaluate whether the borrower’s personal income supports that same monthly payment — regardless of the projected rent.

Two different underwriting lenses. Same property.

Margin Matters

In the example above, the gross spread is roughly $1,700 per month.

But responsible analysis goes further.

Investors should consider:

-

Vacancy

-

Maintenance

-

Capital reserves

-

Insurance increases

-

Property tax adjustments

-

Unexpected repairs

A property that technically qualifies under DSCR does not automatically mean it is resilient.

At the $1M level, especially in Miami, operating costs can shift meaningfully. Margin matters.

When a DSCR Structure May Make Sense

A DSCR loan may align with investors who:

-

Are self-employed

-

Have income that fluctuates or is commission-based

-

Own businesses that reduce taxable income through deductions

-

Are building multi-property portfolios

-

Prefer purchasing through an LLC

-

Want underwriting based primarily on asset performance

For these investors, property-based qualification may better reflect how their finances are structured.

When It May Not Be Ideal

A DSCR structure may be less appropriate if:

-

You qualify easily for conventional financing at a lower rate

-

Your primary objective is minimizing cost of capital

-

The property barely meets minimum DSCR requirements

-

You plan to refinance in the short term (many DSCR loans include prepayment penalties)

-

You lack sufficient liquidity beyond the down payment

DSCR loans typically involve:

-

Higher interest rates than conventional loans

-

Down payments of 20–25%

-

Possible prepayment penalties

These are structural features — not defects — and should be evaluated strategically.

Is It More Expensive?

Often, yes — compared to conventional financing.

But cost cannot be evaluated in isolation.

For some investors, flexibility, scalability, and alignment with their income structure justify the pricing difference.

For others, conventional financing may be more efficient.

The important question is not:

“Is DSCR better?”

The more relevant question is:

“Does this structure align with my financial profile and long-term objectives?”

Questions to Consider Before Pursuing a DSCR Loan

Before choosing this structure, ask:

-

Does the property generate healthy margin beyond the minimum DSCR requirement?

-

Am I comfortable with the interest rate relative to projected returns?

-

Does my income structure make conventional financing restrictive?

-

Do I have sufficient reserves beyond the required down payment?

-

Am I prioritizing portfolio growth or lowest possible borrowing cost?

These are strategic decisions — not product comparisons.

Final Perspective

Conventional financing evaluates your income today.

A DSCR structure evaluates what the property is expected to generate in the future.

It is not a universal solution.

And it is not the only alternative to traditional underwriting.

It is one financing structure among several that informed investors understand and use when appropriate.

In a market like Miami — entrepreneurial, dynamic, and capital-driven — clarity matters more than trends.

The strategy should fit the investor.

Not the other way around.