Mortgage rates have started to ease, and many homeowners are asking the same question:

Should I refinance now—or wait for a better rate?

With political and economic uncertainty in the background, it’s understandable to feel hesitant. But refinancing has never been about predicting the future perfectly. As I’ve written before, interest rates move in cycles—and most people only recognize the “perfect” moment after it has passed.

The better question isn’t “Will rates drop more?”

It’s: Will refinancing improve my total cost and support my personal plan?

And if selling is on your radar—whether that’s next year or several years out—your timeline matters more than the headlines, because refinancing has costs, and those costs have a clock.

1) Start With the “Why”: What Are You Trying to Accomplish?

Refinancing can make sense for several reasons, but the math and strategy change depending on your goal.

Common refinance objectives include:

-

Lowering your monthly payment (by lowering the rate, extending the term, or both)

-

Reducing total interest paid (often by refinancing into a shorter term or a significantly lower rate)

-

Switching loan types (FHA to conventional to remove mortgage insurance, or ARM to fixed for stability)

-

Accessing cash (cash-out refinance for high-interest debt or major home improvements)

-

Removing a co-borrower (if you qualify)

Before you look at rates, be specific about your objective.

Clarity here prevents rate-chasing that doesn’t actually improve your financial outcome.

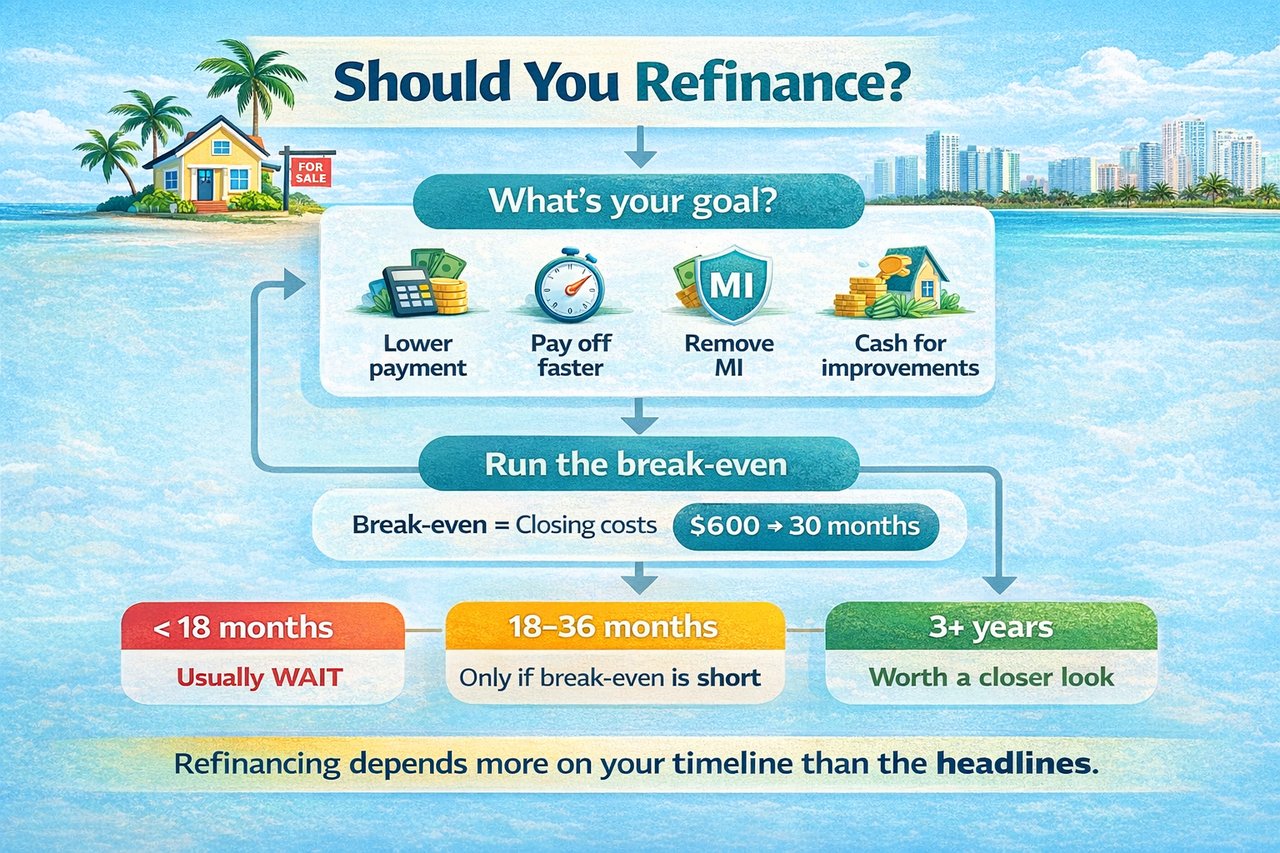

2) The Key Metric: Your Break-Even Point

A refinance comes with costs—lender fees, appraisal, title, and sometimes points. The critical question is:

How long will it take for the monthly savings to repay those costs?

That’s your break-even.

Break-even (months) = Total closing costs ÷ Monthly payment savings

Example:

-

Closing costs: $6,000

-

Monthly savings: $200

-

Break-even: 30 months (2.5 years)

A refinance is usually more compelling when:

-

You expect to keep the home (or loan) longer than the break-even period

-

The savings are meaningful, not marginal

-

You’re not trading a small payment drop for a much longer payoff timeline—unless that’s intentional

Seller lens:

If you might sell in the next 12–24 months, break-even becomes the deciding factor. Refinancing and moving before you recapture the costs can reduce your net proceeds, even if the new payment looks attractive.

3) How Big of a Rate Drop Is “Worth It”?

You’ve probably heard rules like “refinance when rates drop 1%.” That guideline is oversimplified. The real answer depends on your loan balance, remaining term, and time horizon.

That said, refinancing often makes sense when:

-

You can lower your rate by ~0.50%–1.00%+, or

-

You can eliminate PMI or FHA MIP, or

-

You can shorten the term without payment shock, or

-

You’re replacing high-interest debt through a conservative cash-out plan

On larger balances, even smaller rate reductions can work—especially if mortgage insurance is removed.

4) What You’re “Resetting”: Term and Total Interest

One common mistake is focusing only on the monthly payment.

If you refinance a loan you’ve been paying for years into a new 30-year mortgage, you may lower the payment but increase total interest by restarting the amortization clock.

Two ways to protect against this:

-

Refinance into a shorter term (20 or 15 years), if affordable

-

Or refinance into another 30-year loan but continue paying your old payment (or extra principal)

This is especially important for homeowners planning to sell in a few years—you don’t want short-term relief that quietly erodes long-term equity.

5) Credit, Equity, and the Approval Reality Check

Even if rates are falling, your personal terms depend on underwriting.

Stronger refinance candidates typically have:

-

Solid credit profiles

-

Adequate equity

-

Stable income and manageable debt-to-income ratios

-

Clean payment history

Changes in home value since purchase can help—or hurt—depending on your equity position.

6) When Refinancing Often Makes Sense as Rates Decline

Refinancing is usually worth a closer look if you:

-

Have a rate noticeably above today’s market and plan to stay put

-

Want to eliminate mortgage insurance

-

Have an ARM and want stability before the next adjustment

-

Want to restructure your loan term

-

Need cash for a high-ROI renovation with a clear plan

Seller-focused example:

Using refinance funds to update a dated kitchen or refresh a primary bath (counters, lighting, fixtures, paint) can meaningfully change buyer perception later. Homes that feel updated and “easy” often see stronger offers and fewer repair concessions—protecting your negotiating position when you sell.

7) When Waiting May Be the Smarter Move

Refinancing may not pencil out if:

-

You’re planning to sell soon

-

The rate improvement is small and closing costs are high

-

You already have a very low rate and are refinancing mainly for cash-out

-

You’d significantly extend your term without a strategic reason

-

Your credit or equity profile would lead to unfavorable pricing right now

Sometimes improving those factors first is the better move.

8) “Should I Refinance Now or Wait for Rates to Drop More?”

When rates are declining, the temptation is to wait for the bottom. The problem: nobody can time rates perfectly—and waiting has a cost if you’re currently overpaying.

A practical approach:

-

Run the numbers at today’s rate

-

Identify your break-even point

-

Decide based on your timeline and goals

-

If close, ask about options like float-downs or thoughtful cost structures

The right refinance is the one that improves your outcome—even if rates dip another quarter point later.

Quick Refi Decision Checklist

Refinancing may make sense if you can say “yes” to most of these:

-

I plan to keep the home at least ___ years

-

My new loan would save me $___ per month

-

My break-even is ___ months

-

I’m not unintentionally adding significant total interest (or I have a plan to offset it)

-

The refinance supports a clear goal (payment, payoff, MI removal, stability, renovation, or sale strategy)

Final Thought:

Refinancing isn’t about guessing the market. It’s about aligning the numbers with your timeline, plans, and eventual exit. When those line up, the decision becomes much clearer—no matter what the headlines say.